Value-Added Poultry Products: India’s Growth Story at Home and Abroad

Dr. Narahari, Project Consultant – Meat and Poultry

Founder, NH ProPOWER Consultancy Services, Bengaluru, Karnataka

+91 96633 76040, drnarahari@nhpropower.com

Introduction

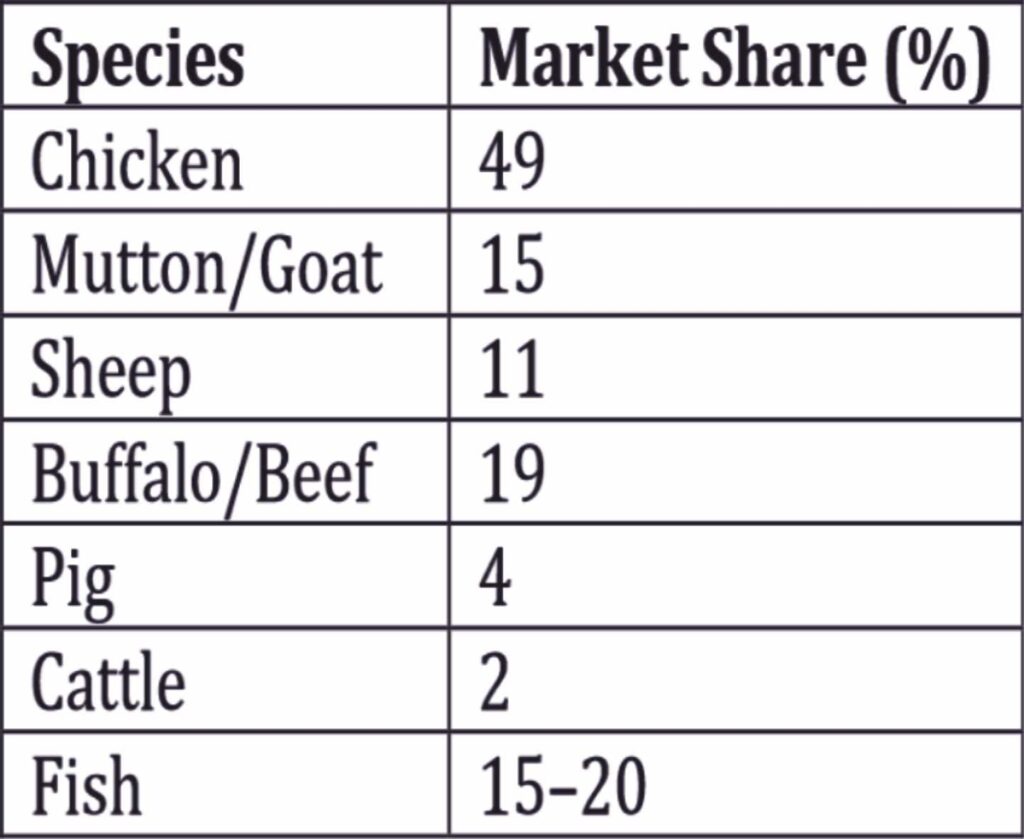

The poultry market reached USD 30.46 billion in 2024. India’s poultry sector has moved far beyond backyard activity and the sale of live birds or fresh cuts to integrated commercial systems. This shift over the last three to four decades, especially in broiler meat and eggs (Annual growth rates: 8–10% for broilers and 4–6% for eggs), is driven by rising incomes, urbanization, modern retail, quick commerce, QSR growth, better cold-chain facilities, and higher protein demand. Value-added poultry products have created space in the industry. They capture premium margins and meet the needs of busy lifestyles by offering convenience, consistency, safety, and branding. Per capita consumption climbed from 0.4 kg in 1980 to 3.2 kg in 2023, and is projected to reach 5 kg by 2030. Poultry dominates India’s edible meat market with 43.78% share in 2025 (USD 6.61 billion). Chicken accounts for about 49% of total meat production. Eggs generate INR 1,500 billion in annual sales (138 billion units).

Table: Market Share of meat production in India

Evolution of India’s Value-Added Poultry Products

From the 1990s to the early 2000s, branded poultry products characterized by basic further processing emerged. A marked phase of accelerated transformation in value-added poultry products occurred in the 2010s. The first large-scale commercialization of products such as nuggets, patties, and sausages was made possible by the rapid expansion of quick-service restaurants (QSRs) and modern organized retail, advances in processing technology, and cold-chain logistics. In the 2020s, the convergence of quick-commerce platforms, direct-to-consumer (D2C) meat brands, and substantial investments in integrated cold-chain infrastructure has significantly reshaped consumption patterns, positioning ready-to-cook (RTC) and ready-to-eat (RTE) poultry products as routine components of urban household food baskets, rather than niche or occasion-based offerings.

Major Value-added poultry Product categories

Value-added poultry in India can be clustered into the following.

1. Breaded & coated products: Products in which marinated or portioned meat is coated with batter and/or breadcrumbs to provide texture, flavor, and moisture retention, typically followed by par-frying or full cooking and freezing for consistent quality, extended shelf life, and convenience across QSR, foodservice, and retail channels. Eg, nuggets, popcorn, fingers, schnitzel, patties.

2. Emulsion-based products: Finely comminuted poultry formulations in which meat proteins, fat, water, and seasonings are emulsified into a stable matrix, then filled into casings or molds and cooked to produce uniform-textured items. Eg, sausages, frankfurters, mortadella-style, cold cuts.

3. Marinated/RTC products: Raw, portioned chicken items infused with spice blends, marinades, or functional ingredients to enhance flavor, tenderness, and cooking performance, enabling quick preparation while retaining fresh-meat characteristics for retail, QSR, and home-consumption markets. Eg, peri-peri cuts, tandoori, biryani cuts, kebab mixes

4. RTE (Ready to eat) products: Fully cooked, thermally processed items that require no further cooking and can be consumed directly or after minimal reheating, offering assured food safety, consistent sensory quality, and extended shelf life for institutional, retail, and convenience-driven consumers. Eg, curries, biryani bowls, grilled chicken strips, etc.

Market Size Ambiguity and Urban Demand Concentration in India’s Value-Added Poultry Segment

Value-added poultry consumption in India is most pronounced in regions with strong cold-chain infrastructure, organized modern retail, and high last-mile delivery penetration. Bengaluru, Delhi-NCR, Mumbai, Hyderabad, Chennai, Pune, and Kolkata consistently emerge as the primary demand centers for organized ready-to-cook (RTC), ready-to-eat (RTE), and direct-to-consumer (D2C) meat distribution. For instance, Licious has publicly emphasized its strong metro-centric presence and phased expansion strategy across leading urban markets. In the states, notably Karnataka, Telangana, Tamil Nadu, and Maharashtra, exhibit higher adoption of RTC and frozen poultry products, while the NCR belt, along with Punjab and Haryana, benefits from strong institutional and QSR demand coupled with expanding organized retail. Meanwhile, eastern metros such as Kolkata are witnessing a gradual scale-up, enabled by quick-commerce platforms and smaller pack formats tailored to emerging urban consumption patterns.

India-specific estimates for sausages and breaded products vary widely across reports due to differences in category definitions, data sources, and methods. For instance, one report places the frozen food market at around INR ~3,500 crore within its defined scope, reflecting an optimistic outlook driven by rising demand for convenient foods. However, such figures should be interpreted as directional indicators rather than absolute market sizes, as reporting boundaries frequently diverge, variously aggregating or separating frozen vegetables, frozen RTC meals, frozen snacks, and frozen meat products. This lack of standardization complicates direct comparisons across reports and underscores the need for cautious interpretation when assessing the scale and growth potential of India’s value-added poultry segments.

Sausages and Breaded Products Market

Sausages and breaded nuggets are growing at a 5.14% CAGR and are valued at approximately USD 380 million by 2031. The total sausages market is around INR 5,000 crore. Breaded products are sold through QSRs like KFC and McDonald’s, with thousands of tonnes sourced annually in India. Southern states lead in the consumption of such products, followed by Haryana, West Bengal, and Uttar Pradesh.

Ready Meals Market

RTC and RTE offerings in India are no longer confined to vegetarian convenience foods; within the meat segment, RTC growth is particularly pronounced in marinated chicken cuts, kebabs and tandoori preparations, biryani-ready mixes, and burger–patty products. RTC and RTE segments grow 15-20%, led by ITC, Venky’s, and Suguna. Also, the segment is valued at ~INR 2,000 crore, driven primarily by strong institutional demand from QSR chains such as Domino’s and KFC, alongside rapid growth in online food delivery platforms like Swiggy and Zomato.

Major players in India’s value-added poultry market

India’s value-added poultry market involves large integrators, FMCG and food companies, D2C brands, and QSR-linked processors, creating a layered supply and demand system. At the core, major integrated players like Suguna Foods, Skylark Hatcheries, Sneha Group, and VH Group offer scale, raw material security, and processing for organized value addition. In branded RTC and frozen products, Godrej Yummiez (under Godrej Agrovet) has a strong line-up of nuggets, pops, and patties. Venky’s has long been in processed chicken and RTC formats sold via organized retail.

Larger food companies like ITC join through RTE food offerings and regional partnerships. Specialist brands such as Prasuma and Keventer, along with many regional firms, have strong positions in sausages, cold cuts, and related products. D2C and omnichannel brands, led by Licious, focus on city-centric scaling, cold-chain control, and RTC selections. This shows the rising importance of digital distribution in value-added poultry.

Equipment Strategy in India’s Value-Added Poultry Sector

Value-added poultry production relies on distinct and more complex equipment, encompassing integrated modules for slaughtering, evisceration, chilling, deboning, portioning, forming, marination or injection, batter–breading, thermal processing, freezing, and advanced packaging with in-line inspection systems. Global market analyses frequently identify multinational suppliers as leading providers of highly automated meat and poultry processing solutions, particularly for high-throughput further-processing applications, as reflected in industry summaries. In parallel, India has developed a broad base of domestic manufacturers and system integrators supplying semi-automatic lines, utilities, and stainless-steel fabrication, including conveyors, chillers, scalders, basic evisceration systems, and balance-of-plant equipment. However, India-specific market share data by supplier origin are rarely disclosed in a citable form. A practical industry view indicates that capital-intensive, high-automation further-processing and sophisticated packaging systems remain largely import-driven, whereas fabrication-heavy, semi-automatic, and utility-focused components are predominantly Indian-supplied.

Export opportunities for value-added poultry products

Export opportunities for value-added poultry are strongest where Indian processors can offer regulatory-compliant and certified production facilities (such as HACCP, ISO 22000, or BRCGS, depending on market requirements), alongside consistent portioning, IQF formats, and cooked or frozen products tailored to institutional and foodservice buyers. In particular, the Middle East and Southeast Asia demonstrate sustained demand for reliable frozen and processed poultry supply chains, positioning compliant Indian value-added processors for selective, yet meaningful, export growth. At present India’s value-added poultry exports are strategically aligned with markets that demand Halal-compliant, cooked, and frozen products, supported by certified processing infrastructure and consistent quality. The Middle East countries, Saudi Arabia, United Arab Emirates, Kuwait, Oman, and Qatar, remain the largest destination, driven by a strong preference for Halal cooked and frozen poultry. Southeast Asian markets such as Vietnam, Malaysia, Singapore, and Philippines focus on institutional and foodservice demand. African destinations, including Ghana, Congo, Angola, and Benin, import price-sensitive frozen and further-processed products. South Asian countries, Nepal, Bhutan, and the Maldives, benefit from the proximity-driven trade, while premium niche markets such as Japan and Hong Kong source products with high-specification, value-added, and institutional poultry products.

Opportunities: Dried meats and pickles

This segment remains underexploited yet culturally well aligned with Indian consumption habits, offering significant scope for scalable growth in value-added animal protein products. Its expansion potential is supported by shelf-stable formats, which substantially reduce dependence on continuous cold-chain infrastructure, alongside strong regional taste preferences for spice-forward and traditional flavor profiles. These attributes make the segment well-suited for travel snacking, gifting, and export to diaspora markets. Product opportunities include dried or jerky-style chicken strips formulated with Indian masala blends, smoked and dried poultry snacks, retort-processed pickles in pouches or jars, and dry snack variants inspired by coastal and North-Eastern cuisines. Commercial success in this category depends on precise control of water activity, validated thermal processing protocols for retorted products, and carefully designed preservative strategies, complemented by high-barrier packaging systems to prevent oxygen and moisture ingress. Equally critical are regulatory compliance, food safety validation, and, where feasible, clean-label positioning to ensure both consumer trust and long-term market sustainability.

Conclusion

India’s value-added poultry growth is best understood as the convergence of convenience with rising protein aspirations, enabled by advances in cold-chain infrastructure, branding, and processing technologies. Domestically, continued expansion is expected as organized RTC and RTE products move beyond metros into tier-2 cities, supported by smaller pack sizes and quick-commerce platforms. Internationally, while the opportunity space is more selective, it remains tangible in markets where India can reliably deliver consistent quality, regulatory compliance, and cost-competitive processed poultry products.

References are available on request.